Financial Literacy: Teaching Kids How To Buy A Home

Homeownership has become a hard-to-reach goal for many young adults. The rising costs of houses coupled with high student loan debt mean some young people don’t have the same buying power as their parents did. And with COVID-19 continuing to disrupt our economy, it could make it even harder for young adults to save money moving forward.

Adding further credence to this is that people in their early 20s have 20% less disposable income than the national average. Because of the financial hurdles many young adults face now, it’s vital for parents to teach their kids financial literacy – and start them early.

For parents, helping your child buy a house begins with giving them the tools they need to develop a strong understanding of personal finance. This baseline financial literacy can give them confidence that they have the information they need to make smart money choices. This guide will help parents develop an educational blueprint to help their kids achieve a better position for homeownership.

Financial literacy for kids means giving your children an all-round education on money management. While each family’s financial circumstances are unique, there are valuable lessons available in all home budgets. Use your home’s budget to tailor a plan to help your children learn more about personal finance. And it’s never too early to begin this process with your child.

Financial literacy for kids means giving your children an all-round education on money management. While each family’s financial circumstances are unique, there are valuable lessons available in all home budgets. Use your home’s budget to tailor a plan to help your children learn more about personal finance. And it’s never too early to begin this process with your child.

As your child grows, they’ll have more things occupying their time: school, sports, a copious amount of homework, and other extracurricular activities. While this might be a harder time to grab their attention, it’s also a pivotal time to do so. One effective way to establish communication is to find something they’re interested in as a launching off point. In many cases, this could be them preparing for college. Once you have their attention, here’s how to teach them more about financial literacy:

As your child grows, they’ll have more things occupying their time: school, sports, a copious amount of homework, and other extracurricular activities. While this might be a harder time to grab their attention, it’s also a pivotal time to do so. One effective way to establish communication is to find something they’re interested in as a launching off point. In many cases, this could be them preparing for college. Once you have their attention, here’s how to teach them more about financial literacy:

Now that you have worked with your child to build a financial foundation, it’s important for them to take the lessons they learned and make smart decisions. With an uncertain financial future, it is vital to maintain that dialogue with your child and be a resource they can turn to, not only if they need money, but as they make decisions that shape their financial future.

Now that you have worked with your child to build a financial foundation, it’s important for them to take the lessons they learned and make smart decisions. With an uncertain financial future, it is vital to maintain that dialogue with your child and be a resource they can turn to, not only if they need money, but as they make decisions that shape their financial future.

The importance of financial literacy throughout a child’s life

Financial literacy for kids means giving your children an all-round education on money management. While each family’s financial circumstances are unique, there are valuable lessons available in all home budgets. Use your home’s budget to tailor a plan to help your children learn more about personal finance. And it’s never too early to begin this process with your child.

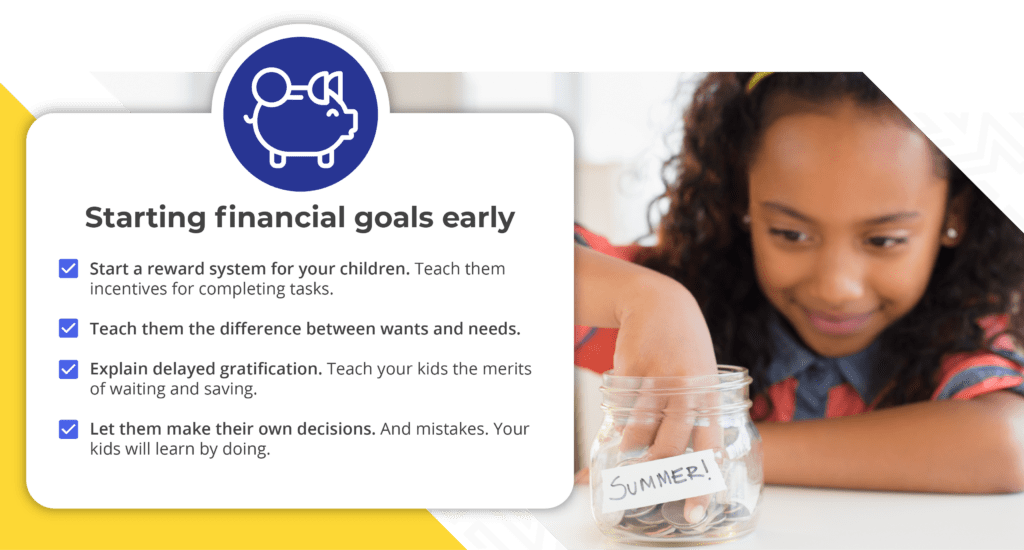

Start financial goals early

You might think your children are too young to talk about money. However, they’re at the age where they absorb everything. This is your chance! While you have their attention, start a dialogue about money. Sure, you won’t break down investments over espressos with your five-year-old, but these tips can help you develop a blueprint to educate them over time:- Start a commissions/reward system for children: You can teach them the value of incentives by giving them commissions or rewards for completing tasks. Start with small chores such as folding the laundry or cleaning the dishes. Once they have completed the task, they earn stickers, a toy, a coin, or something else of their choosing. The goal is to help them develop a sense of ownership for completing a task.

- Distinguish the difference between wants and needs: Show your children the difference between things you need such as food, water, and shelter versus things that are nice to have but are not necessary, like a big TV. Next, take them on a shopping trip. Give them a specific amount of money they can use to buy what they want within that budget. Doing this exercise opens up a dialogue between you and your child about how money is a limited resource while helping them understand what items cost.

- Time helps money grow: Have your child set their sights on something they want to buy that’ll take a few weeks of chores to earn. Instead of them spending their money each week, they learn to save it, with the reward of earning the item after they have enough money saved. Another option is for them to have a clear piggy bank, so they see the benefit of saving every time they add money. This practice helps them understand that it’s sometimes beneficial to delay instant gratification.

- Allow children to take ownership: It’s hard to relinquish control as a parent, but it’s also good as your child needs the freedom to make their own decisions. The reason for this is you want them to learn through doing even if they make mistakes.

Resources

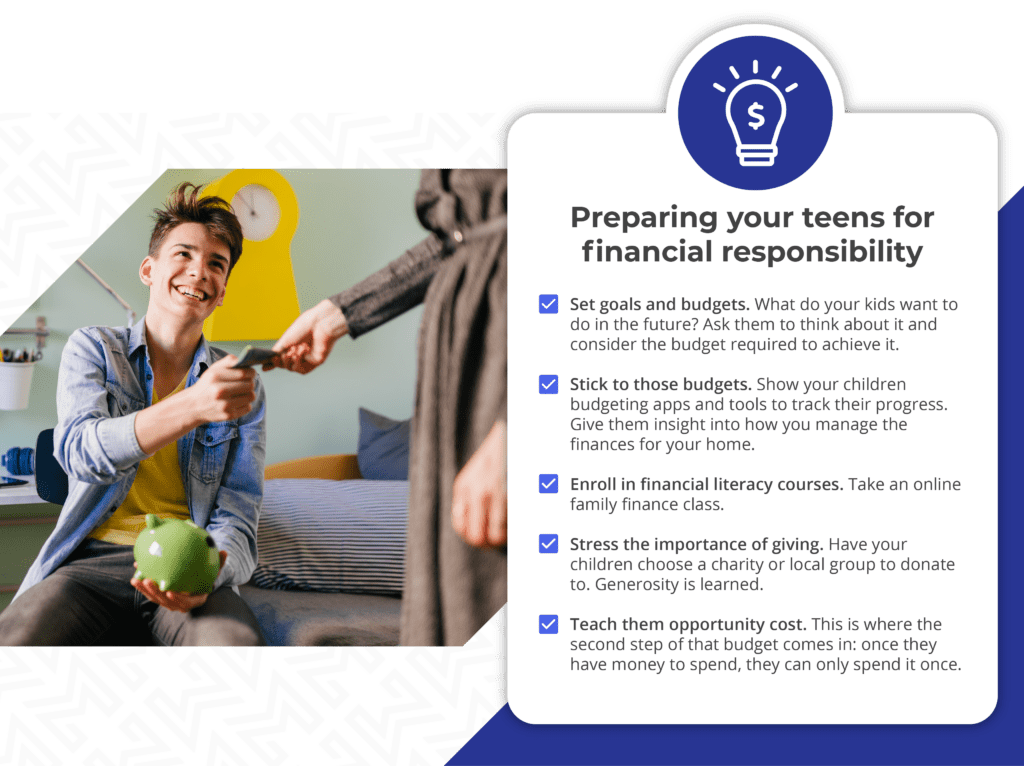

Preparing your teens for financial responsibility

As your child grows, they’ll have more things occupying their time: school, sports, a copious amount of homework, and other extracurricular activities. While this might be a harder time to grab their attention, it’s also a pivotal time to do so. One effective way to establish communication is to find something they’re interested in as a launching off point. In many cases, this could be them preparing for college. Once you have their attention, here’s how to teach them more about financial literacy:

- Create/set goals: What does your child want to do in the future? The simple act of asking this question shows them they have ownership in their decisions. It also gives you the chance to stress the importance of budgeting the money they earn and saving a portion of it to reach their goals.

- Practice budgeting: Once they have some money, have them use the budgeting app EveryDollar, as it helps you and your child have a discussion on the importance of budgeting. You can also show them the budgeting apps or tools you use and give them their first look into your household’s budget and how you maintain it.

- Maintain or start a commission/reward system: If you haven’t implemented a reward or commission system yet, now is the time to do so. Helping your child buy a house faces a crucial building block at this stage: They are learning to work towards something bigger in the future. It also helps them gain ownership and see money is earned.

- Enroll in financial literacy courses: For some reason, many high schools don’t offer personal finance courses. Because of this, it’s ideal to enroll your child in a financial literacy course. Some local banks and credit unions offer a chance for teens to either take online classes or come in for a day to learn how money works. This is also essential for helping your child buy a house, as it gives your kids the tools they need to make smarter financial decisions.

- Stress the importance of giving: Along with saving and budgeting, giving money is also a vital part of personal finance. Have your children choose a charity, local group, or church to donate money to. Doing this teaches them the importance of being generous.

- Allow children to take ownership: Give your children the freedom to make some of their financial decisions. Doing this helps them see the benefits of their behaviors and when they make mistakes, it teaches them valuable lessons now while they still have a safety net.

- Show opportunity costs: This is where your child has to weigh decisions. Do they spend their money on a new phone or saving that money for college?

Resources

- Check out your local credit union for financial literacy courses

- Use budgeting apps like EveryDollar

- Play some financial literacy games

- Teach your kids to donate to a charity of their choice

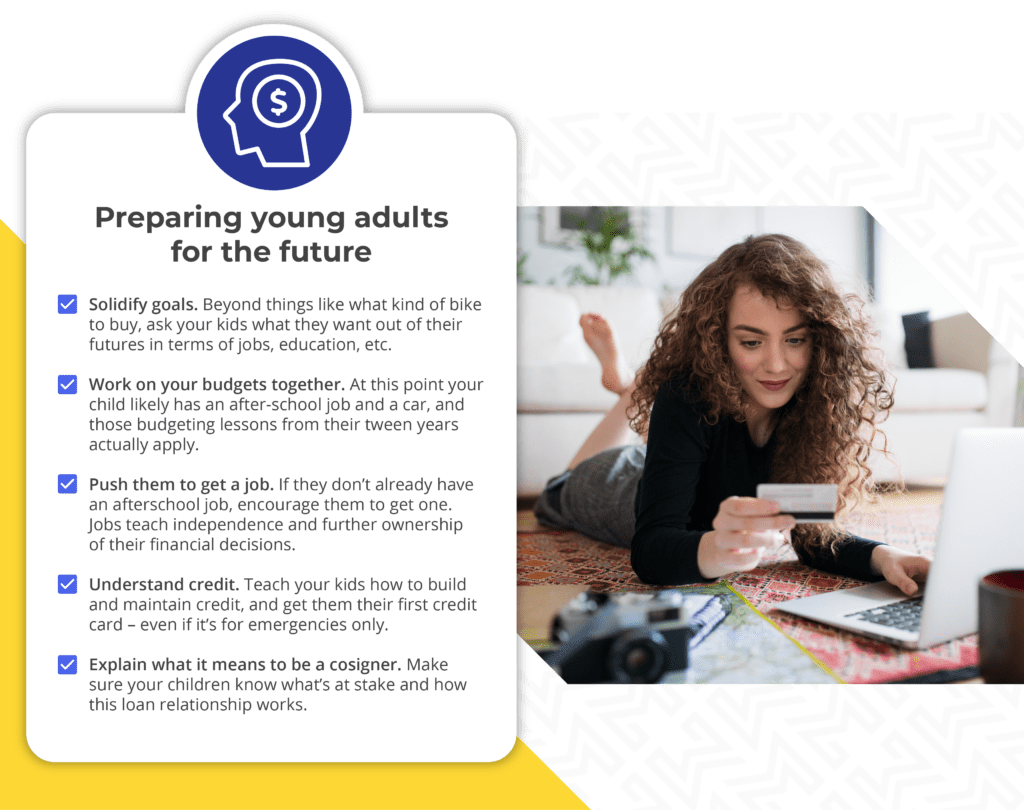

Prepare young adults for the future

Now that you have worked with your child to build a financial foundation, it’s important for them to take the lessons they learned and make smart decisions. With an uncertain financial future, it is vital to maintain that dialogue with your child and be a resource they can turn to, not only if they need money, but as they make decisions that shape their financial future.

- Continued education: It’s important your child knows the value of re-learning the basics and discovering new things. Offer to take a financial literacy class with them. Make it fun, where both of you go through this journey together. Afterwards, you can discuss anything new you learned. Overall, this is a great way to keep the dialogue ongoing.

- Start to solidify goals: As part of this dialogue, ask your children what their future holds and ways they plan to achieve their goals. This is where you can also share your goals and ways you plan to achieve them. By continuing this transparency, it helps your child feel more comfortable opening up about their finances.

- Budgeting: Budgeting now is easier than it ever has been. There are many free apps available that track budgets for you. Chances are, even your bank or credit union has online tools to help you budget. Again, strive for transparency with your child by showing them how you budget and what you do if you overspend on one category (i.e. taking away Dad’s Bass Pro Shop credit card.) You could even set up a time monthly to work on your budget together. This helps your child understand the importance of budgeting and by working on this together, you both build accountability.

- Savings: When having these talks, it’s vital you stress the importance of saving their money. Explain to them that by starting earlier in life, they’ll be able to build more wealth over time through compound interest. If you’ve done well in this regard, feel free to share with them statements from your broker over the years showing how your money has grown.

- This is also a good time to speak with them about opening a 401k or another retirement savings vehicle. And when it comes to buying a house, explain to them how the bigger of a down payment they can make, the lower their monthly payment is. This is why it’s important for them to begin now to save for the future whether that includes homeownership, going back to school, or even starting their own business.

- Understanding credit: This is one of the most important aspects of financial education. Talk to your children about the importance of building credit the right way as their score can affect how much they spend on a car, house, and even insurance.

- Break down the components that make up your credit score such as payment history, debt to income ratio, and more. You can also help them develop best practices such as paying off your credit card balance every month, paying all bills on time, and keeping your total debt to income ratio to under 30% if at all possible.

- During this time, if you made any mistakes with credit such as charging too much or being late with payments, talk to them about it, telling them how much time it took to rebuild your score. Having this discussion is one of the most important ways your child can see how your credit score impacts a lot of future financial decisions you’ll make.

- Jobs: Another part of teaching kids real estate and responsibly homebuying is explaining to them the importance of a stable job history. Even if they live at home, having a job gives them independence and ownership over their financial decisions. It also provides them with the opportunity to save some of their money. During these discussions, explain to them how if they bounce around from job to job or don’t work for longer periods, it could make it more difficult to receive a job offer or mortgage preapproval in the future, especially in the current market.

- Cosign or co-borrower: In some cases, you might want to help your child establish their credit or even help them buy their home. You can talk to them about being a cosigner on their loan and how this helps them earn a lower interest rate. However, it’s also important to stress this shouldn’t be a crutch your child relies on all the time. Instead, it’s to help them build a good payment history at favorable rates so they won’t need you in the future. It’s also important for both of you to discuss the pros and cons of this approach. The pros are your child is more likely to receive approval and their interest rate will be lower if your credit is good. The downside is if they are late on the payments, the lender will require you to pay them.

- Parents providing further assistance: Since families’ finances are unique to them, it’s important to weigh many considerations here. In some instances, the unfortunate reality is you might not be able to help your children with a downpayment or cosigner assistance. If this applies to you, it’s okay, just be upfront and honest with your children so their expectations are aligned with reality.

- In other instances, you might be able to help them with a down payment. This is huge, as it’s difficult for millennials to save enough money to even afford a down payment. And in some rarer cases, the parent might be able to buy the house for the child or have the child move into a home the parent owned.

- Parents could also provide monthly payments to help out with the mortgage or any repairs that arise. The key here is to create balance and set expectations upfront before going into this endeavor with your child. Explain to them what you’re able or unable to do that way they know from the outset the expectations placed on them.

Resources

- Helping your child buy a house requires budgeting tips

- Tips on how to save

- Pointers for building credit

- And some steps for how to have difficult money conversations